Emerging markets (EM) debt, which performed well for most of 2024, lost momentum in the fourth quarter due to uncertainty about the new U.S. administration’s policy agenda, inflation concerns, and monetary policy repricing.

We now believe EM debt credit spreads are more indicative of fair valuations. While high-grade credit spreads are below long-term averages, high-yield credit spreads are still marginally above long-term averages. Moreover, the spread between high-yield EM debt and high-grade EM debt (as well as U.S. corporate high-yield credit) remains above long-term averages.

While EM debt credit spreads are clearly less appealing than they were in 2023 and early 2024, yield levels remain attractive, in our opinion, driven by higher underlying U.S. Treasury yields. Therefore, we expect EM hard currency debt returns in 2025 to be driven predominantly by lower U.S. underlying Treasury yields and carry, and less by credit-spread compression.

Our favorable outlook for the 10-year U.S. Treasury yield has not changed since the U.S. elections, and we continue to believe that there are attractive opportunities for investors to increase exposure to long-duration securities to lock in attractive real and nominal yields.

We also expect favorable technical conditions, and 2025 should be another year of subdued new net debt issuance. And we could see positive flows into the asset class as higher yields drive investors back to fixed income in a U.S. Federal Reserve (Fed) rate-cutting cycle.

We continue to see marginally better value in high-yield, high-beta credit and remain positioned for further high-yield/investment-grade credit spread compression. That said, we believe the distressed/defaulted universe should present fewer investment opportunities as most defaulted countries have restructured. Furthermore, we do not expect EM sovereign credit defaults over the next year.

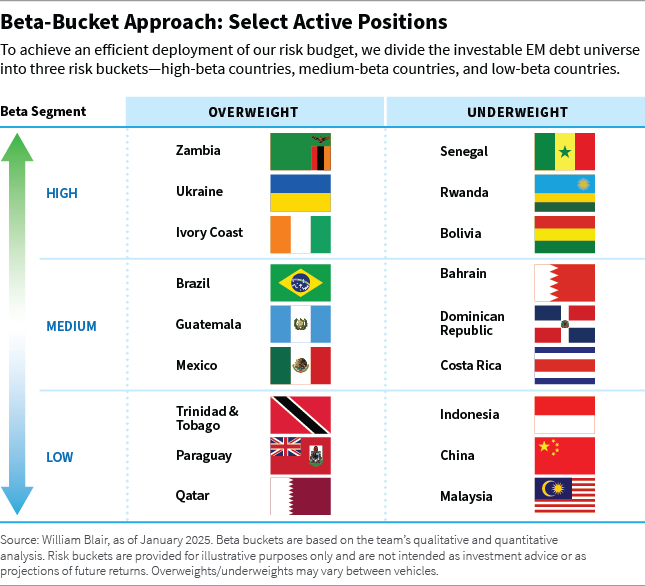

Below, we break down some of our largest active positions by beta bucket, which is how we allocate our risk budget.

High-Beta Bucket

In the high-beta bucket, our largest overweight positions are in Zambia, Ukraine, and Ivory Coast, while our largest underweight positions are in Senegal, Rwanda, and Bolivia.

Zambia (overweight): Valuations appear favorable and the fundamental outlook is positive. We believe 2025 is likely to show improved agricultural performance and energy availability as rains bring much-needed relief. Activity in the mining sector should also support copper output, in our view.

Ukraine (overweight): There is the potential for conflict negotiations, multilateral support, and a more optimistic growth outlook in 2025. We express this view through an overweight to warrants, but have recently reduced our allocation to the B bonds based on valuations.

Ivory Coast (overweight): We are overweight euro-denominated hard currency bonds due to attractive valuations and our view that the country fundamentally is on a path of improvement. Authorities appear committed to prudent fiscal policies, supported by strong backing from development partners.

Senegal (underweight): Public debt and fiscal deficit figures have been revised upward for the past five years, with sharp fiscal underperformance in 2024. The 2025 budget’s fiscal consolidation faces significant implementation risks. While bond valuations have improved, we see limited potential for outperformance without credible policy measures to restore fiscal credibility.

Rwanda (underweight): Our lack of a position is the result of tight valuations and fundamental concerns about the size of Rwanda’s twin deficits.

Bolivia (underweight): Our underweight is largely due to credit concerns. The policy mix of large fiscal deficits and a pegged exchange rate appears unsustainable amid low reserves, a current account deficit, and 2024’s foreign currency shortages. Valuations are not compelling enough to justify a position given the country’s weak fundamentals, in our opinion.

In Brazil, we have shifted corporate credit exposure toward sovereign positions.

Medium-Beta Bucket

In the medium-beta bucket, our largest overweight positions are in Brazil, Guatemala, and Mexico, while our largest underweight positions are in Bahrain, Dominican Republic, and Costa Rica.

Brazil (overweight): We increased exposure late in the fourth quarter, finding valuations attractive despite a weaker fundamental outlook. While the budget deficit raises concerns, it primarily impacts local currency debt, as Brazil’s liabilities are mostly denominated in the real. We have shifted corporate credit exposure toward sovereign positions.

Guatemala (overweight): The country has what we consider attractive valuations and strong fundamentals, including low debt, stable deficits, and robust growth, all of which support a positive ratings trajectory.

Mexico (overweight): We favor Pemex for its sovereign backing and attractive valuations relative to the sovereign. We also maintain positions in Mexican financials and airlines. However, we are underweight the Mexico sovereign because we don’t find the valuations compelling.

Bahrain (underweight): We are concerned about volatility in regional geopolitics, the country’s weak fiscal-reform efforts, lower oil prices, and tight valuations.

Dominican Republic (underweight): Although the country appears to be on a positive fundamental trajectory, we do not find valuations compelling.

Costa Rica (underweight): Fundamentals are strong, but we find valuations unattractive because spreads have compressed materially.

Low-Beta Bucket

In the low-beta bucket, our largest overweight positions are in Trinidad and Tobago, Paraguay, and Qatar, while our largest underweight positions are in Indonesia, China, and Malaysia.

Trinidad and Tobago (overweight): We recently moved to an overweight position due to the country’s more appealing valuations relative to its low-beta peers.

Paraguay (overweight): We believe the country has attractive valuations relative to low-beta peers. We also find its fundamentals solid: the country’s debt-to-gross-domestic-product ratio remains low and the country has a strong history of low fiscal deficits.

We believe Qatar is the most resilient market in the region in case of falling oil prices due to its lower fiscal breakeven.

Qatar (overweight): We believe Qatar is the most resilient market in the region in case of falling oil prices due to its lower fiscal breakeven.

Indonesia (underweight): We find valuations unappealing, and the outlook appears uncertain following the February 2024 presidential elections. With the new government prioritizing growth over stability, fiscal slippage risks have increased. Indonesia is expected to be a significant external debt issuer in 2025. However, we maintain diverse corporate positions, supported by resilient fundamentals in financials, renewable utilities, and oil and gas.

China (underweight): Valuations are tight, and Chinese state-owned entities have unpredictable regulatory risks. Based on a bottom-up analysis, we hold selective corporate bonds at attractive valuations and positive credit trajectories.

Malaysia (underweight): Valuations are unappealing. Although the country’s economic growth remains robust, supported by resilient exports and strong private consumption, and fiscal consolidation efforts are ongoing, the spreads for Malaysia’s sovereign bonds are among the lowest in the index.

Marco Ruijer, CFA, partner, is a portfolio manager on William Blair’s emerging markets debt team.