Despite softer economic conditions globally, emerging markets (EM) credit fundamentals remain supportive—and while we see some pockets of weakness, especially among energy- and food-importing countries, overall we believe EM debt is well positioned to withstand a period of weaker global growth.

You can read more about our economic outlook in our last blog post, Emerging Markets Debt: Clearer Skies Ahead?, In terms of strategic opportunities, we favor high-yield issuers over high-grade issuers and remain strategically overweight in higher-yielding frontier markets, where we believe investors are overcompensated for credit risk and volatility.

We continue to see scope for fundamental differentiation among countries. We prefer high-yield commodity-exporting countries, especially in the energy space. We also remain cautious about countries that depend on food and energy imports and countries with negative political dynamics that create institutional risks. We also prefer countries with easier access to financing, especially those that have strong relationships with multilateral and bilateral lenders.

We continue to see opportunities in select distressed debt positions, where we believe bond prices do not reflect realistic assumptions for default risk and recovery values. We also see selective opportunities in EM corporate credit, where we believe a combination of differentiated fundamental drivers, favorable supply technical conditions, and attractive absolute valuations could continue to provide ample investment opportunities.

Given near-term growth concerns and intermittent primary markets, we are focusing on issuers with low refinancing needs and robust balance sheets. In Latin America, our positions are diversified across oil and gas; technology, media, and telecommunications (TMT); utilities; and financials. In Central and Eastern Europe, the Middle East, and Africa (EMEA), our positions are diversified across financials; oil and gas; metals and mining; and real estate. In Asia, our positions are diversified across oil and gas; financials; industrials; metals and mining; utilities; and real estate.

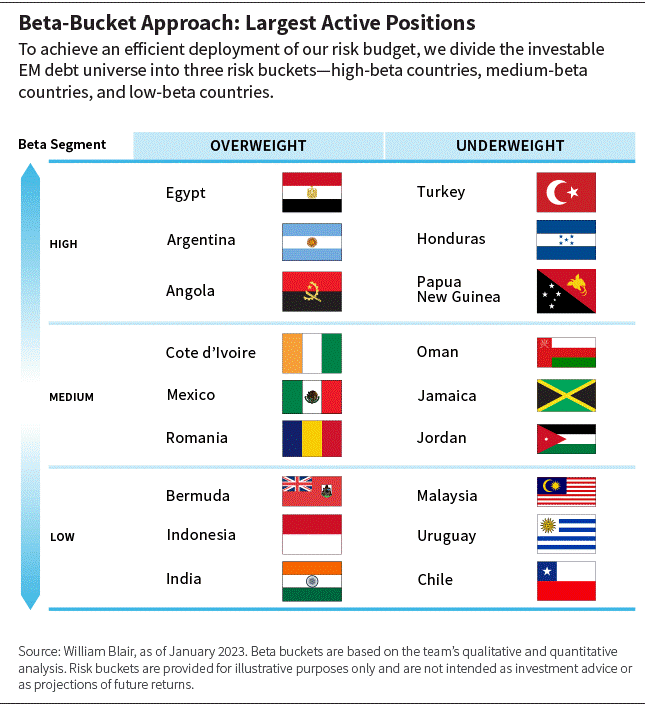

Our highest-conviction overweight and underweight positions are shown in the table below.

High-Beta Bucket

In the high-beta bucket, our largest overweight positions are in Egypt, Argentina, and Angola, and our largest underweight positions are in Turkey, Honduras, and Papua New Guinea.

Egypt (overweight): We believe external financing needs will be met with support from partners in the Middle East and the International Monetary Fund (IMF). Critically, we believe the recent currency adjustments will, moving forward, reduce imbalances and support increased financial inflows.

Argentina (overweight): Overall, we remain bearish about Argentine fundamentals, although we believe sovereign bonds are priced below eventual recovery value, providing potential value. We favor bonds on the curve with stronger indenture protections. We remain overweight via higher-quality provincial issuers. We have also purchased credit default swap (CDS) protection (net) to hedge against a default by the Argentine government.

Angola (overweight): We believe in Angola’s prudent policies. The exchange rate flexibility demonstrated in the past quarter cements our view.

Turkey (underweight): Imbalances and unsustainable policies continue to erode the country’s creditworthiness. We believe political uncertainty is likely to remain elevated in coming months given the prospect of elections. Our exposure remains concentrated in long-dated, low-price cash bonds, with our exposure in spread-duration terms closer to neutral.

Honduras (underweight): We do not believe that valuations properly reflect fundamentals. Although Honduras has the capacity to service its debt, fundamentals have been declining. The electricity sector, in particular, has been mismanaged, which has created fiscal challenges. The new government has threatened repudiation of its debt obligations, which gives us some concerns about Honduras’s willingness to pay. Given valuations and the small chance of debt repudiation, we believe there is better value elsewhere.

Papua New Guinea (underweight): A low foreign-exchange (FX) reserves base and a weak fiscal position lead us to avoid the country, although the debt maturity profile is well spaced out (mostly to bilaterally lenders).

Medium-Beta Bucket

In the medium-beta bucket, our largest overweight positions are in Cote d’Ivoire, Mexico, and Romania, and our largest underweight positions are in Oman, Jamaica, and Jordan.

Cote d’Ivoire (overweight): We find attractive valuations in long-dated euro-denominated bonds and believe fundamentals remain relatively supportive.

Mexico (overweight): Our overweight is largely in the state-owned energy company Pemex, which offers one of the largest spreads over its sovereign, and we believe could benefit from the high likelihood of support from the sovereign.

Romania (overweight): We see improving fundamentals and strong relative valuations. We continue to prefer euro-denominated issues over U.S.-dollar-denominated bonds but continue to look for value in U.S.-dollar-denominated bonds in the new-issue market.

Oman (underweight): Oman has been a strong reform story over the past couple of years, but we believe this story is now fairly priced in. The country still has a high dependency on oil, whose prices are vulnerable to slowing global growth.

Jamaica (underweight): Jamaica has continued to implement an impressive fiscal consolidation agenda, even following the pandemic. Despite kicking the debt-to-GDP target can down the road due to pandemic impacts, fiscal discipline has resulted in continued fundamental improvement. However, we believe market expectations are too high and high dollar prices on many Jamaican bonds lead us to believe there is more efficient allocation of capital elsewhere.

Jordan (underweight): Valuations look stretched on a relative basis given the weak outlook for growth, high levels of debt, and need for further improvement in the fiscal dynamics.

Low-Beta Bucket

In the low-beta bucket, our largest overweight positions are in Bermuda, Indonesia, and India, and our largest underweight positions are in Malaysia, Uruguay, and Chile.

Bermuda (overweight): We favor the country’s valuations and fundamentals relative to other low-beta sovereigns. Bermuda has similar valuations to Peru and Chile, but a stronger fundamental trajectory because there is less institutional uncertainty in Bermuda.

Indonesia (overweight): Indonesia has experienced improved terms of trade and structural reforms. Its economic fundamentals have strengthened in recent years through credible policymaking and prudent fiscal policies. The country has attracted foreign direct investment inflows, and our positioning aims to capture opportunities from green projects and value-chain developments in the country.

India (overweight): India has strong fundamentals. It is relatively insulated from external demand compared to other low-beta sovereigns, with resilient domestic demand supporting economic growth. Credit growth remains robust, and we expect inflation to moderate and slow the pace of central bank rate hikes.

Malaysia (underweight): We see unappealing valuations, typically in the longer-duration sovereign and quasi-sovereign bonds.

Uruguay (underweight): Fundamentals remain strong, but bonds have compressed materially since the COVID-19 pandemic, and we believe this offers limited potential spread tightening.

Chile (underweight): Valuations are tight and the political trajectory is uncertain. After the failed approval of a new constitution, we believe institutional uncertainty lingers and there are more attractive markets in which to invest.

Marco Ruijer, CFA, partner, is a portfolio manager on William Blair’s emerging markets debt team.