Due to increasing index concentration in the market, passive funds do not have the ability to actively address the risks associated with their disproportionate exposure to the largest index constituents and are essentially betting on the future success of a limited group of companies.

William Blair’s Large Cap Growth strategy’s disciplined focus on risk management combines a meticulous portfolio-construction process that seeks to guard against unintended risks in an evolving market landscape. The portfolio does not take outsized factor or macro bets, but rather is constructed so that idiosyncratic risk at the stock level is the main driver of performance.

We believe our mindful approach to managing benchmark-relative risk, and our focus on investing in “structurally advantaged” companies, gives us the potential to consistently outperform the large-cap growth universe of managers.

Investors Face Unintended Passive Risk in the Large-Cap Growth Asset Class

While large-cap indices have delivered strong returns relative to other asset classes over the last decade, index concentration has risen over this period as the largest index constituents have become an increasingly sizable portion of the large-cap asset class and have been outsized contributors to index performance.

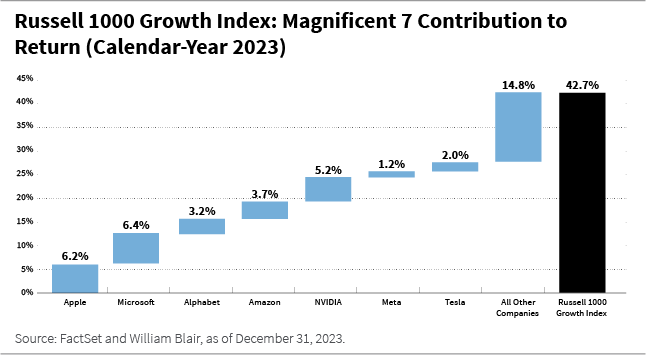

For example, in 2023, the Magnificent 7 stocks (Apple, Alphabet, Amazon, NVIDIA, Meta, Microsoft, and Tesla) represented approximately 47% of the Russell 1000 Growth Index[1] weight as of year-end and accounted for approximately 65% of the contribution to return for the index, as shown in the chart below. Said differently, the performance of the index was driven by a small number of stocks.

Passive funds do not have the ability to actively address the risks associated with their growing exposure to these prominent constituents as market concentration increases. Large-cap passive funds have become top-heavy, with their growing exposure to the largest index constituents moving in tandem, systematically allocating escalating weights to stocks with the highest market capitalizations in accordance with their respective indices.

As a result, passive investors are increasingly reliant on the future success of a limited group of companies. Notably, since the latter half of 2023 and into the beginning of 2024, the index has experienced a moderate decoupling of performance; several of the Magnificent 7 stocks have lagged the broader index return.

This period has also coincided with a deterioration in the performance ranking of the index versus the large-cap growth universe of managers—a sign that the relative performance of active managers versus the index has improved.

In contrast, active managers are not bound by the dominant weights in the index and may be well positioned to navigate an evolving market landscape. Put differently, active managers can strategically position their portfolios to capitalize on the best opportunities. This is in contrast to their passive counterparts who are reliant on the continued success of a limited set of stocks in the index.

William Blair’s Large Cap Growth strategy’s portfolio-construction framework is designed to mitigate unintended risks. Accordingly, it has produced consistent risk-adjusted returns over time. In addition, we believe investors can benefit from a more intentional focus on active large-cap growth investing to help grow and protect their assets.

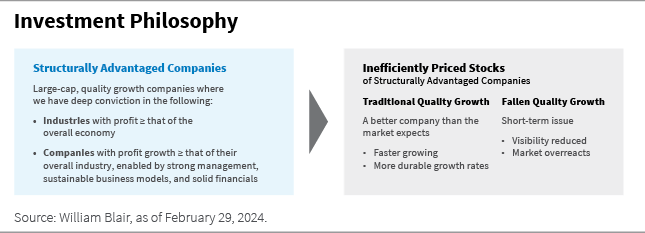

Our Large-Cap Growth Investment Approach: Finding Structurally Advantaged Companies

William Blair’s expertise in quality growth investing has spanned many decades. Specifically, within the large-cap space, we employ our structurally advantaged framework, which helps us identify growing large-cap companies in growing industries.

Our investment process is driven by a research-intensive approach where we seek to identify mispricings or inefficiencies in the large-cap growth marketplace. As a result, we are able to find structurally advantaged companies whose stock we believe is mispriced relative to the company’s long-term earnings growth potential and the durability of that growth.

The first step to identifying structurally advantaged companies is our industry assessment. We seek to identify industries that we believe have strong, long-term secular growth drivers in place and invest in growing companies within those industries.

As an example, we view digital advertising to be a secular growth industry. Advertisers are increasingly shifting to more targeted and trafficked digital options to disseminate ads, allowing digital advertising to continue to take share from more traditional avenues, such as printed media and linear television.

However, while we hope every industry in which we invest will exhibit an upward growth trajectory over the long term, we are cognizant that some structurally advantaged industries tend to be more cyclical than others. These cyclical industries have secular growth characteristics but a greater level of cyclicality than purely secular growth industries, such as digital advertising. This may result from the overall economic cycle or a cycle native to that particular industry.

As one might expect, a critical factor when investing in more cyclical industries is identifying where the industry is in its cycle. For instance, we believe the semiconductor industry provides an attractive growth opportunity with long-term secular tailwinds, including the increasing use of generative artificial intelligence (AI) and the transition to 5G networks. However, we consider semiconductors to be a cyclical growth industry, leading us to reduce or add to our exposure as we track and evaluate the current position in the cycle.

Once we identify what we view to be growing industries, we seek to identify companies that are taking share of industry profit pools, have the right management teams in place, and operate efficient and sustainable business models that have the potential to boost their competitive advantage over time. We believe this focus enables us to identify the best opportunities within each sector and across market cap segments and improves the consistency of relative returns over time.

Regardless of where we are in the broader economic cycle, our focus is on investing in quality growth companies in growing industries that we believe can outperform the market and create long-term alpha. The result is a portfolio that consists of 30 to 40 structurally advantaged companies that are diversified across sectors and market-cap segments.

Our Large-Cap Growth Portfolio Construction: Managing Risk Through Diversification

William Blair’s Large Cap Growth strategy combines a distinct approach to stock selection with a meticulous portfolio-construction process. The primary objective of our portfolio-construction process is neutralizing undesirable risks while allowing the driving force of portfolio returns to be stock selection.

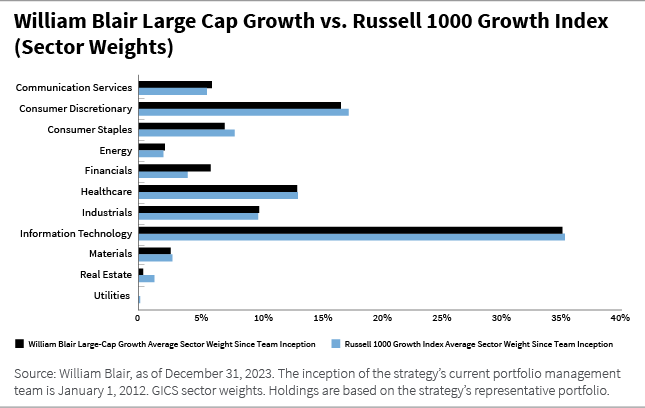

Sector and market-cap diversification is an important element of managing unintended risk and reducing volatility in our portfolio. We believe having material underweights or overweights across sectors or market- cap segments has the potential to negatively impact benchmark-relative returns, as performance across these segments of the benchmark tends to widely fluctuate over time due to the impact of macro events and other sector-specific factors.

In order to minimize this risk, we aim to maintain sector and market-cap neutrality over time such that our alpha is largely driven by stock selection in the long term. As illustrated in the chart below, our sector exposures in the portfolio have been approximately in line with the Russell 1000 Growth Index since team inception, which has limited the volatility of benchmark relative returns and provided a smoother experience for investors.

However, having sector weights that are approximately in line with the benchmark does not mean our strategy has a low active share. Over the past five years, the average active share of the strategy has been approximately 65%.

Furthermore, our sector-neutral approach does not extend to our industry exposures, an area in which we believe we add significant value as active managers. As discussed above, we not only examine a company’s position within its industry, but also the industry itself as we do our diligence throughout our intensive research process.

We seek to identify and invest in industries whose profits are growing at least as fast as, or ideally faster than, the overall economy. This typically leads us to industries that have strong secular growth tailwinds and are positioned on the right side of change for long-term growth.

For example, we have found that the biopharmaceutical industry does not currently fit into our structurally advantaged framework. While large-cap companies in the biopharmaceutical industry may benefit from sizable revenue streams stemming from their approved drugs in the intermediate term, patent issues typically become a significant deterrent to long-term growth because companies are forced to transition from branded to generic pricing. Given that this dynamic negatively impacts a company’s long-term growth potential, we have been consistently underweight the industry relative to our index.

This research-intensive approach and portfolio-construction framework culminates in a portfolio designed for idiosyncratic risk at the stock level (such as security-specific risk) to be the predominant contributor to portfolio risk and returns over time. This allows our competitive advantage, deep company knowledge, and robust bottom-up research to help be the main drivers of performance over the long term. We believe this leads to consistent return potential, as the predominant source of our active risk is taken at the stock level and not driven by outsized sector or factor bets that can introduce excess volatility.

In addition, we seek to build individual positions with positive active overweights ranging from 100 to 350 basis points relative to the Russell 1000 Growth Index. We consider this to be a key differentiator relative to other large-cap growth managers. Importantly, we do not “closet index” the portfolio by taking partial positions in stocks relative to the index. This element of our portfolio construction underscores the deep conviction we hold in each stock within the portfolio.

Finding the Right Manager

William Blair’s Large Cap Growth strategy offers a conviction-based portfolio of 30 to 40 holdings that are diversified across sectors and market-cap segments but has had a risk profile more akin to diversified peers with a larger number of holdings.

Out of the 297 strategies in the Nasdaq eVestment large-cap growth universe, William Blair’s Large Cap Growth strategy is one of only a small number of managers that provides a fundamental approach to large-cap growth investing, more than $5 billion in assets under management (AUM), low long-term tracking error, and less than or equal to 40 portfolio holdings.

Our quality-growth framework and portfolio-construction approach are designed to mitigate the volatility of benchmark-relative returns over the long term. We believe our portfolio offers the potential for stronger risk-adjusted returns and less volatility than the large-cap growth universe.

In Summary

We believe William Blair’s Large Cap Growth strategy offers the potential for consistent long-term performance. Our philosophy of investing in structurally advantaged companies, coupled with our portfolio construction approach that prioritizes stock selection and seeks to guard against unintended risks, seeks to achieve strong risk-adjusted returns over the long term to help grow client assets.

Aaron Socker is a portfolio specialist on William Blair’s U.S. growth and core equity team.

Aden Gebeyehu is an associate portfolio specialist on William Blair’s U.S. growth and core equity team.

[1] The Russell 1000 Growth Index is an unmanaged index registered to Russell/Mellon. It measures those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. It is a capitalization-weighted index as calculated by Russell on a total return basis with dividends reinvested. Indices are unmanaged and do not incur fees or expenses. A direct investment in an unmanaged index is not possible. Index performance is provided for illustrative purposes only. Past performance is not indicative of future results.

Active share is a measure of the percentage of holdings in a portfolio that differ from a benchmark index.

Tracking error measures the extent to which a portfolio tracks its benchmark.