We anticipate a strong 2024 for emerging markets (EM) debt on the back of a significant improvement in the global macro backdrop.

While it appears likely that the global economy will continue to gradually decelerate, we believe growth should remain close to its long-term potential. In such an environment, central banks in advanced economies have likely reached the end of their hiking cycles, and many EM central banks have already started cutting policy rates.

The increased likelihood that the global monetary tightening cycle is nearly over leads us to believe that there are attractive opportunities for investors to start adding to duration to lock in attractive real and nominal yields. In this context, we are looking for opportunities to increase allocation to longer-duration securities.

We see ample opportunities in EM frontier and distressed credit.

We continue to see value in high-beta, high-yield credit and are positioned for high-yield/investment-grade spread compression because we believe the global market environment will be conducive to the outperformance of high-beta, high-yield credit.

We also see scope for fundamental differentiation. We prefer countries with easier access to multilateral and bilateral funding. Multilateral and bilateral support to EMs remains strong and could make a meaningful contribution to external funding in 2024. In this context, we see ample opportunities in EM frontier and distressed credit.

Meanwhile, the corporate credit space continues to exhibit a combination of differentiated fundamental drivers, favorable supply technical conditions, and attractive relative valuations to select sovereign curves. We are seeking investment opportunities where corporate credit fundamentals and attractive spreads coincide. Short-maturity bonds have outperformed, but opportunities in longer bonds are beginning to appear. We continue to focus on issuers with low refinancing needs, robust balance sheets, and positive credit trajectories.

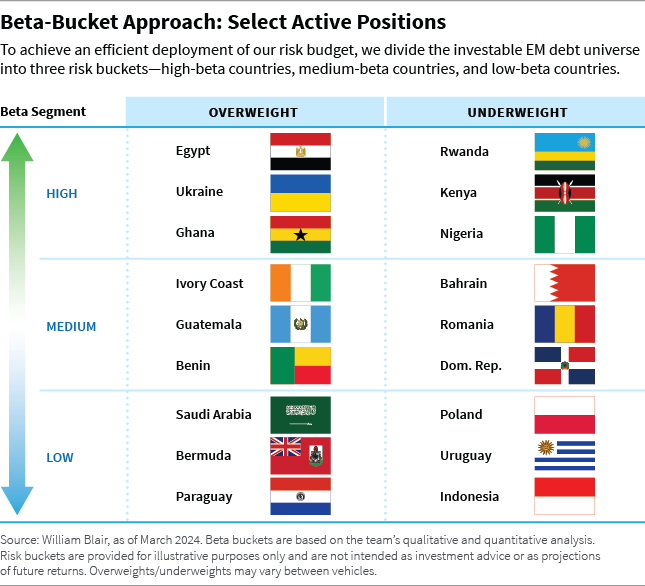

Below, we break down some of our largest active positions by beta bucket, which is how we allocate our risk budget.

A View of the Potential Opportunities: Overweight/Underweight

High-Beta Bucket

In the high-beta bucket, our largest overweight positions are in Egypt, Angola, and El Salvador, and our largest underweight positions are in Nigeria, Kenya, and Honduras.

Egypt (overweight): We believe Egypt’s external financing needs will be met with support from partners in the Middle East and the International Monetary Fund (IMF). We see scope for Egypt to catch up to the broader move in high-yield credits and believe valuations are attractive.

Angola (overweight): Angola has attractive valuations, and we believe authorities’ commitment to fiscal consolidation and broader economic reform is genuine. Moreover, the depreciation of the kwanza demonstrates commitment to a flexible exchange rate, in our view. We believe this will serve the economy well over the medium term.

El Salvador (overweight): In our view, it is likely that President Nayib Bukele, one of the most popular politicians in Latin America, will be reelected in February. This could provide the political cover to reach an agreement with the IMF (although one potential obstacle is the country’s adoption of bitcoin as legal tender).

We remain concerned about governance issues within Honduras, which lead us to believe there is better relative value elsewhere.

Nigeria (underweight): Nigeria has tight valuations relative to peers. After strong performance in the immediate aftermath of the elections, we are looking for signs of more cohesive policies and full implementation of reforms announced earlier this year.

Kenya (underweight): Spreads have tightened to levels at which we believe there is better value in other high-beta names. There have been some conflicting statements from authorities as to how maturing 2024 bonds will be financed, the twin deficits remain wide, and ongoing currency weakness is likely to persist in the near term, in our opinion. IMF support should, however, ensure that there is not a default event on the upcoming maturity.

Honduras (underweight): We do not hold any Honduran bonds because we do not like the valuations, given fundamental risks. Although Honduras has the capacity to service its debt in the near term, credit fundamentals have been declining. The electricity sector has been particularly mismanaged, creating additional fiscal challenges. Overall, we remain concerned about governance issues within Honduras, which lead us to believe there is better relative value elsewhere.

Medium-Beta Bucket

In the medium-beta bucket, our largest overweight positions are in Benin, Guatemala, and Brazil, and our largest underweight positions are in Oman, Costa Rica, and Turkey.

Benin (overweight): We see value in Benin relative to other more liquid sub-Saharan names. Reform momentum remains strong, and Benin continues to enjoy a strong relationship with the IMF. Robust growth, relatively low levels of public debt, and ongoing fiscal discipline led Benin to receive an upgrade from Standard & Poor’s in the last quarter of 2023, and the outlook is now rated “positive” (up from “stable” previously).

We believe Guatemalan President Juan José Arevalo will likely face political obstacles when he assumes office, but Guatemala will remain a strong credit.

Guatemala (overweight): Political noise has increased following President Juan José Arevalo’s win in the August elections, as some branches of government have taken an aggressive stance toward Arevalo’s Semilla party, raising concerns about the stability of the transition period. However, we still believe Arevalo will assume office in January and the electoral process will be respected. Arevalo will likely face political obstacles when he assumes office, but we believe that due to strong initial conditions in the country via strong leverage ratios and low fiscal deficits, Guatemala will remain a strong credit, as it has strong macroeconomic conditions and attractive valuations.

Brazil (overweight): We continue to hold diversified positions across several sectors in Brazil and have been adding through the new-issue market as well. We currently hold seven issuers across seven different sectors of the Brazilian economy.

Oman (underweight): A medium-beta-bucket country during the fourth quarter, we upgraded Oman to our low-beta bucket at the end of the year due to its lower volatility and consistently strong performance. Oman has enjoyed a strong fiscal reform story over the past couple of years. However, we believe this story is now priced in. The country is still highly dependent on the oil sector, where prices remain vulnerable to slowing global growth, and we believe there is the potential for the positive reform momentum to stall if oil prices fall below the fiscal breakeven level and remain there.

Costa Rica (underweight): Costa Rica has unappealing valuations, in our opinion. Spreads in Costa Rica are now the tightest they’ve been since 2013.

Turkey (underweight): We see risks ahead of local elections in March, as President Recep Tayyip Erdogan has unexpectedly shifted policy direction before with no advance warning. Valuations also look tight given the recent change in positioning, and the recent large increase in the minimum wage suggests that it is prudent to adopt more of a wait-and-see approach to this market for now.

Low-Beta Bucket

In the low-beta bucket, our largest overweight positions are in Qatar, Poland, and Bermuda, and our largest underweight positions are in Indonesia, Uruguay, and UAE.

Qatar (overweight): We believe issuance is likely to be a key theme for investment-grade countries in the first quarter of 2024, given the dramatic rally in U.S. Treasury yields and EM bond spreads in the last quarter of 2023. Although Qatar may issue opportunistically, we do not expect issuance in as large a size as some of its peers, given Qatar’s strong fiscal position and lower debt levels.

Poland could benefit from the result of last year’s parliamentary elections, which led to a more market-friendly government taking over in December.

Poland (overweight): Although we expect heavy issuance from Poland in 2024, we expect issuance to be skewed largely toward the domestic and euro currency. In our opinion, Poland could benefit from the result of last year’s parliamentary elections, which led to a more market-friendly government taking over in December.

Bermuda (overweight): Bermuda’s bonds have similar valuations to other low-beta sovereigns, such as those of Peru and Chile, but we believe the country has a stronger fundamental trajectory with less institutional uncertainty.

Indonesia (underweight): We underweighted Indonesia after a year of significant spread compression resulted in unappealing valuation compared to its low-beta peers. By the end of 2023, the country’s J.P. Morgan EMBIGD spread was 87 basis points. Based on fundamentals, the outlook is stable, although the presidential election scheduled for February 2024 and risk of new-year supply are impediments to near-term spread performance.

Uruguay (underweight): Credit fundamentals in Uruguay remain strong, but bond prices have compressed materially since the COVID-19 pandemic, and we believe this results in limited scope for additional spread tightening.

UAE (underweight): We find valuations unappealing. Bonds in weaker credits, such as Sharjah and Dubai, have rallied to the point where we believe valuations are no longer attractive relative to fundamentals. We prefer to own positions in real estate issuers at more attractive valuations. Moreover, within the Gulf Cooperation Council (GCC) region, we continue to prefer Qatar to UAE; reflecting this, we hold a relative overweight spread duration position in Qatar. This overweight is driven by the lower issuance needs in this market relative to GCC peers.

Marco Ruijer, CFA, partner, is a portfolio manager on William Blair’s emerging markets debt team.