Despite the recent headwinds from rising U.S. Treasury yields, we have not changed our constructive medium-term outlook for emerging markets (EM) debt.

Duration performed poorly as policy rates around the world sharply adjusted over the past couple of years. At the same time, yield curves were deeply inverted, leaving longer-dated bonds vulnerable to a correction.

However, over the past six weeks, yield curves have dis-inverted significantly. That, coupled with the increased likelihood that the global monetary tightening cycle is nearly over, lead us to believe that there are attractive opportunities to add to duration and lock in attractive real and nominal yields. So, we are seeking to increase allocation to longer-duration securities.

In the sovereign arena, we see value in high-beta, high-yield credit and are positioned for high-yield/investment-grade spread compression. We prefer countries with easier access to multilateral and bilateral funding.

We’re focused on corporate issuers for whom we believe credit quality is unlikely to implode in the higher-for-longer rate scenario.

In the corporate arena, relative outperformance has reduced the opportunity set, but we continue to find investment opportunities in which fundamentals and attractive spreads coincide. We’re focused on issuers for whom we believe credit quality is unlikely to implode in the higher-for-longer rate scenario. Even as rates have risen and refinancing concerns have moved front and center, many issuers have medium-term, low-rate fixed maturities, allowing them to ride out the current rate volatility without major deterioration to credit quality.

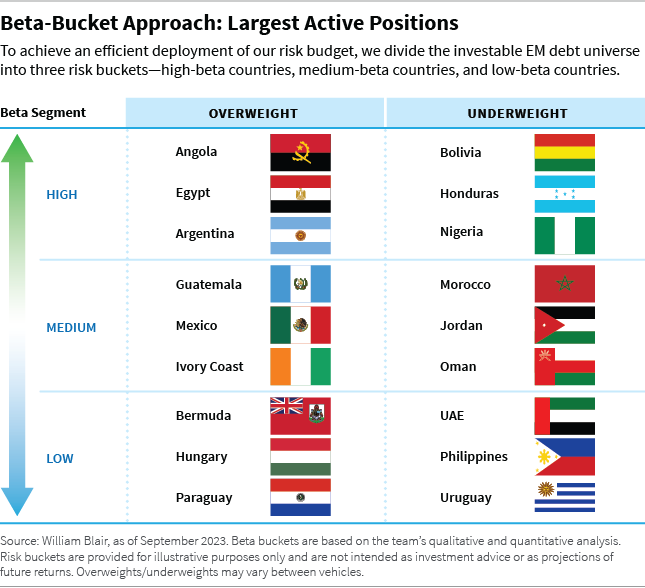

Below we break down our largest active positions by beta bucket, which is how we allocate our risk budget.

A View of the Potential Opportunities: Overweight/Underweight

High-Beta Bucket

In the high-beta bucket, our largest overweight positions are in Angola, Egypt, and Argentina, and our largest underweight positions are in Bolivia, Honduras, and Nigeria.

Angola (overweight): Valuations are attractive in our view, and we believe in authorities’ commitment to fiscal consolidation and broader economic reform. Moreover, the depreciation of the kwanza demonstrates commitment to a flexible exchange rate, in our view. We believe this will serve the economy well over the medium term.

Egypt (overweight): We believe Egypt will meet its external financing needs with support from partners in the Middle East and the International Monetary Fund (IMF). We see scope for Egypt to catch up to the broader move in high-yield credits. Also, valuations appear attractive.

Argentina (overweight): Although a shortage of dollars has led to exceptionally challenging macroeconomic conditions, the outlook appears promising. Although the policy mix has deteriorated over the last month, meaning economic imbalances will have to be addressed sooner than later, it appears increasingly likely that a more pragmatic government will assume office in 2024. We also believe Argentina has the means to remain current on its debt next year. However, the next government will face a challenge in the implementation of reforms needed to address imbalances and maintain social stability.

We are concerned about Bolivia’s unsustainable debt dynamics.

Bolivia (underweight): We are concerned about the longer-term trajectory of Bolivia’s economy as fiscal deficits remain too large and the fixed exchange rate is causing unsustainable debt dynamics.

Honduras (underweight): We do not like the valuations of Honduran bonds given fundamental risks. Although Honduras has the capacity to service its debt in the near term, credit fundamentals have been declining. The electricity sector has been particularly mismanaged, in our view, creating additional fiscal challenges. Moreover, the government has threatened repudiation of the country’s debt obligations, which makes us concerned about Honduras’s willingness to pay. Thus, we think there is better value elsewhere.

Nigeria (underweight): Nigeria’s valuations are tight relative to peers. After strong performance in the immediate aftermath of the elections, we are waiting for signs of more cohesive policies and full implementation of reforms announced earlier this year.

Medium-Beta Bucket

In the medium-beta bucket, our largest overweight positions are in Guatemala, Mexico, and Ivory Coast, and our largest underweight positions are in Morocco, Jordan, and Oman.

Guatemala (overweight): Valuations are attractive and macroeconomic conditions are strong, in our opinion. Political noise has increased following President Bernardo Arevalo’s win in the August elections, as some branches of government have taken an aggressive stance toward Arevalo’s Semilla party, raising some concerns about the stability of the transition period. We still believe President Arevalo will assume office in January and that the electoral process will be respected, but we acknowledge the potential for some additional noise along the way.

Mexico (overweight): Our overweight is primarily via the state-owned energy company, Pemex, which offers one of the largest spreads over sovereign bonds. We believe it could benefit from government support, which appears likely. We also hold several positions in financials and retail, which we believe are poised to benefit from supportive sovereign trends.

Ivory Coast (overweight): We find valuations of U.S.-dollar-hedged, euro-denominated, long-dated bonds attractive, and we believe credit fundamentals are relatively supportive.

We believe Pemex could benefit from government support.

Morocco (underweight): We believe the economy is likely to face fundamental headwinds despite strong official support.

Jordan (underweight): We find valuations unappealing. Jordan has performed well recently given its successful program with the IMF, which is helping reduce the fiscal deficit. However, we believe this progress is now fully priced in, yet there remain significant risks around the pace of fiscal reform. These risks could leave Jordan more vulnerable to a negative shift in risk sentiment given its high level of government debt.

Oman (underweight): Oman has enjoyed a strong fiscal reform story over the past couple of years. However, we believe this story is now priced in and the country still has a high dependency on the oil sector, where prices remain vulnerable to slowing global growth. However, we believe there is the potential for the positive reform momentum to stall if oil prices fall below the fiscal breakeven.

Low-Beta Bucket

In the low-beta bucket, our largest overweight positions are in Bermuda, Hungary, and Paraguay, and our largest underweight positions are in UAE, Philippines, and Uruguay.

Bermuda (overweight): We prefer valuations and fundamentals in Bermuda to those of other low-beta sovereigns such as Peru and Chile. Bermuda has similar valuations but a stronger fundamental trajectory with less institutional uncertainty.

Hungary (overweight): Hungary appears inexpensive within the low-beta opportunity set, particularly now that the latest issuance is behind us. Expectations for economic growth are improving as the central bank continues to ease monetary policy. Moreover, there remains the potential for Hungary to unlock funding from Europe if an agreement with the European Union is reached.

Paraguay (overweight): Valuations have improved and we believe the economy remains in solid shape, and we have increased our exposure to medium-tenor instruments as the shape of the curve has flattened.

Hungary appears inexpensive within the low-beta opportunity set.

UAE (underweight): We remain underweight in UAE because of unappealing valuations. Bonds in weaker credits, such as Sharjah and Dubai, have rallied to the point where we believe valuations are no longer attractive relative to fundamentals. We prefer to own positions in real estate issuers at more attractive valuations. Moreover, within the Gulf Cooperation Council (GCC) region, we continue to prefer Saudi Arabia to UAE; reflecting this, we hold a relative overweight spread duration position in Saudi Arabia. This overweight is driven by the more positive reform momentum story in Saudi Arabia.

Philippines (underweight): Credit fundamentals are weak relative to other low-beta sovereigns, and valuations are unappealing. Technical conditions are also unfavorable as we believe the country is likely to issue new sukuk bonds before the end of the year.

Uruguay (underweight): We find valuations poor. Credit fundamentals in Uruguay remain strong, but bond prices have compressed materially since the COVID-19 pandemic, and we believe this results in limited scope for additional spread tightening.

Marco Ruijer, CFA, partner, is a portfolio manager on William Blair’s emerging markets debt team.