Emerging markets debt held its ground in the first quarter, but staying ahead means staying selective. We’re reassessing positioning across high-, low-, and frontier-beta currencies and rates as trade tensions and U.S. policy inject fresh uncertainty.

A Good First Quarter

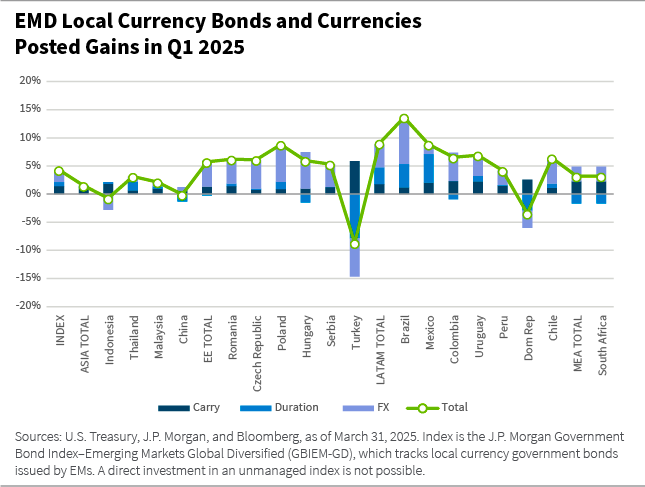

The first quarter of 2025 was characterized by rising uncertainty around the policy agenda of the new U.S. administration, but local currency emerging markets (EM) debt performed well during the period, thanks to a supportive fundamental backdrop in EM countries and a strong tailwind from declining U.S. Treasury yields and a weaker U.S. dollar. The J.P. Morgan Government Bond Index–Emerging Markets Global Diversified (GBIEM-GD) returned 4.31%, with currencies and local rates contributing nearly equally to the top-line result.

A More Cautious Outlook

While we retain a constructive medium- and long-term outlook for EM debt, we have downgraded our near-term views for the asset class, for reasons my colleague Marco Ruijer explained in his blog, “Tariff Tensions and Tactical Shifts in EM Debt.”

In the local currency space, we have steadily reduced net exposure to higher-beta and liquid currencies, vis-à-vis the U.S. dollar, on the view that foreign exchange (FX) will be a significant relief valve for a global trade shock.

That said, this global shock is likely to be different from those we’ve observed in recent decades. It is driven by U.S. policy, and we believe the United States may suffer negative consequences in growth and inflation—possibly more so than EMs.

As a result, in recent weeks we’ve seen relatively strong performance in EM equities and outflows from U.S. assets. If risk sentiment toward local markets holds firm, EM central banks will have more space to cut interest rates without the added risk of currency weakness and higher inflation—a counter-cyclical policy lever that has been underused in recent years.

Among liquid currencies, we prefer relative value positions because there is high variation in initial price and market-positioning conditions, as well as exposure to trade and commodities.

In frontier markets, we have reduced exposure at the margin through hedges in highly exposed currencies, such as the Vietnamese đồng, and idiosyncratic currencies, such as the Argentine peso.

Should global risk conditions continue to deteriorate, we are likely to continue to selectively hedge exposures with currency forwards rather than sell bonds.

Should global risk conditions continue to deteriorate, we are likely to continue to selectively hedge exposures with currency forwards rather than sell bonds.

Conversely, the strategy is broadly overweight duration across emerging and frontier markets, based on the view that the negative growth and inflation shock will have a greater effect on bond prices than on spreads or the country-risk component of term premiums.

As is the case with frontier markets, we prefer to hedge rate risks with derivatives (selective country credit default swaps and options on EM spreads) rather than sell bonds at distressed levels and with elevated transactions costs.

Overall, we believe our strong focus on risk management and diversification should help us mitigate downside risks during market turmoil.

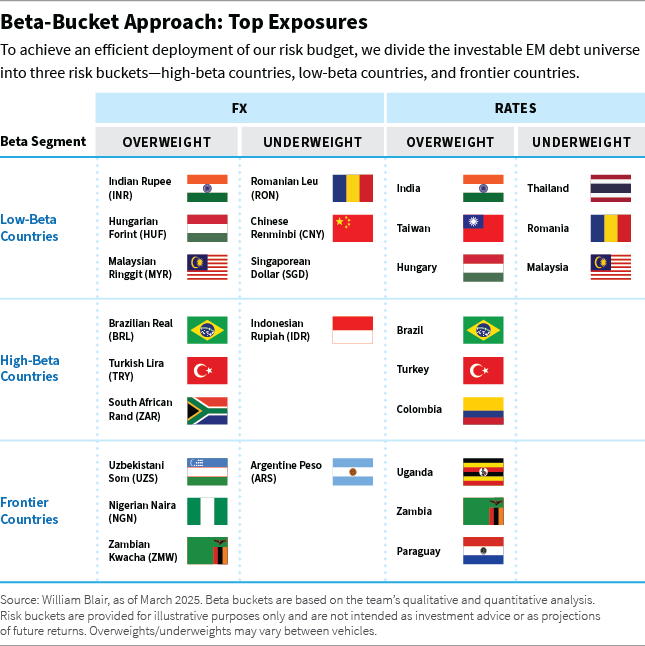

Below, we break down some of our largest active positions by beta bucket, which is how we allocate our risk budget.

Low-Beta Bucket

In the low-beta bucket, we hold an overweight duration position in India and the rupee. Our duration overweight is due to declining inflation dropping to within the central bank’s target range. Liquidity injections by the central bank and a supportive bond-supply calendar should further support yields declining in India.

In Hungary, we are overweight the forint due to attractive valuation relative to the Polish zloty and the relatively higher carry. Although the Hungarian central bank is one of the most aggressive in the region, we believe that Hungary is now closer to the terminal rate than other markets in the region. In bonds, our overweight in Hungary duration was concentrated largely in a green bond. Real rates are attractive, in our opinion, and although they are now closer to the terminal rate, the central bank has been one of the most progressive in the region. Renewed focus across Europe on meeting excessive deficit targets may help moderate the size of the fiscal deficit in the coming period in spite of the wider acceptance that Europe needs to raise defense spending.

In Malaysia, we remain overweight the ringgit. Economic growth remains robust, supported by resilient private consumption. Fiscal consolation efforts are ongoing. The currency outperformed last year but remains inexpensive on a trade-weighted basis. The central bank has encouraged state-linked companies and exporters to convert foreign currency to help support the ringgit, though these flows may only resume after global trade uncertainties diminish. We are underweight Malaysia duration as valuations are unappealing. Domestic demand has remained resilient even as the external environment has become more uncertain.

In Romania, we hold an underweight position in the leu as we have concerns about the twin deficits, particularly during an election cycle. We are awaiting a rerun of the presidential election this year, and the coalition has not delivered on a strong fiscal consolidation plan. The currency is also overvalued, in our opinion, contributing to a lack of competitiveness in the region and a large current account deficit.

We are underweight the Chinese renminbi because of the potential for additional tariffs being imposed on China by the U.S. administration.

We are underweight the Chinese renminbi because the potential for additional tariffs being imposed on China by the U.S. administration keeps us cautious. While the central bank has fixed the currency stronger to limit depreciation expectations, an escalation of trade tensions will likely lead to depreciation pressure increasing.

We are underweight the Singapore dollar on rich valuations and low carry. Furthermore, Singapore is a trade-oriented country that may be sensitive to changes in external demand.

In Taiwan, we hold an overweight duration position as rate hikes are priced in. Inflation remains low at approximately 2%. We believe economic growth should decline toward potential growth in 2025 as export growth normalizes after a robust 2024.

We are underweight Thailand duration because valuations are unappealing. Rate cuts are already priced in, but financial stability concerns may lead to fewer central bank cuts than are currently priced in.

High-Beta Bucket

We have reduced directional FX exposure to the dollar across the portfolio in favor of relative value exposures within EMs.

In this regard, our overweight position in the Brazilian real is paired with an underweight position in the Chilean peso. We believe that risks in Brazil are more fully priced in for both the currency itself and real short-term interest rates following significant tightening by the central bank. Brazil also has a relatively closed economy and lower exposure to U.S. trade risks. While the Chilean peso is similarly inexpensive against the dollar, low real interest rates and elevated macro exposure to global growth and copper prices make the currency vulnerable to weak external conditions.

In Turkey, although political volatility has increased, the economic reform path remains intact, allowing strong performance in many economic indicators, such as current account and FX reserve levels. In our opinion, investors continue to be overcompensated by high yields, which we do not believe will be fully eroded by currency depreciation. Investors may also take a closer look at local bonds as the central bank raised rates in an emergency meeting to help fight currency flight.

Our underweight to the South African rand is more of a tactical play based on strong performance relative to high-beta peers.

In South Africa, we have a small tactical overweight to the rand based on strong performance relative to high-beta peers over recent months. Although the markets were satisfied with the composition of the unity government, its impact on South Africa’s low potential growth rate is likely to be tested by conflicting ideologies, particularly as it pertains to the budget, which has proved difficult to reach consensus on.

We are underweight the Indonesian rupiah on increased concerns about the country’s fiscal outlook. We believe the government is likely to prioritize economic growth over fiscal prudence. The central bank has intervened to reduce the amount of depreciation, but portfolio outflows have persisted.

In Colombia, we increased to a small overweight in rates following a reduction in Mexico. We expect the curve to flatten as the central bank nears the end of its cutting cycle and slower growth, lower commodity prices, and weaker risk appetite weigh on growth and inflation. Current levels of both real interest rates and curve term premium appear attractive relative to both regional and beta-bucket peers.

Frontier Bucket

We have an out-of-benchmark position in Uzbekistan due to high gold prices and a recovering Russian ruble. Gold is an important component of the Uzbek economy and contributes meaningfully to the reserve position and fiscal revenues. Russia remains a key trading partner with Uzbekistan and a stronger ruble will relieve pressure on the competitiveness of the Uzbek economy.

In Nigeria, we maintain our long position in the naira given the attractive carry offered by open-market-operation bills. The decline in oil prices, if sustained, is likely to present a challenge. We therefore remain vigilant about the potential downside risks to this trade.

In Zambia, we maintain our long bond position given the scope for further disinflation in 2025.

In Zambia, we maintain our long bond position given the scope for further disinflation in 2025; this could support performance. While the central bank is likely to remain hawkish in light of short-term risks related to the global backdrop, we see scope for the local currency yield curve to bull steepen.

We continue to hold an underweight in the Argentine peso as valuation pressures rise steadily given the strong appreciation of the currency in real terms. Inflation has fallen significantly, from a year-over-year high of 290% a year ago to above 60% currently. The government has prioritized currency stability ahead of legislative elections due to take place in the fourth quarter. However, we believe that overvaluation, a terms-of-trade shock, and increasingly vulnerable external accounts are likely to force a policy change sooner.

We continue to see value in Uganda local currency assets, and the relatively mature local currency government yield curve also allows us to express this view in longer-dated bonds. We hold a long bond position on attractive real rates, and we have partly hedged our exposure to the Ugandan shilling given our view that the currency is overvalued and vulnerable to a correction.

We added a position in Paraguayan local bonds based on the country’s strong macro fundamentals, favorable inflation dynamics, and low correlation to global risk factors. We believe external accounts may improve with the recent weakening of energy prices, and the currency should be well supported in the near term.

Lewis Jones, CFA, FRM, is a portfolio manager on William Blair’s emerging markets debt team.