The first half of 2025 generated plenty of news flow to worry about, including tariffs, wars, and the Deep Seek moment. Yet, equity markets performed well: developed markets outside the United States returned more than 17%, while the broader U.S. indices returned just shy of 6%, reversing a trend of U.S. dominance over the last several years (see chart below).

We believe collapsing growth differentials are one of the primary explanations for what is happening in the global financial markets. Economic growth in the United States is now expected to be weaker than its four-year recent trend, while the economies of Japan and the euro area may actually accelerate.

As quality growth investors, seeking answers to “where is growth?” and “where is it changing?” remains central to how we invest. We believe quality companies have the ability to exploit opportunities afforded by economic growth, and some actually create new demand (though these are rarer but more valuable).

Wedges are Back

The world outside of the United States has performed significantly better than the United States for the first time in nearly a decade. How can this be when discussions of U.S. exceptionalism are all the rage?

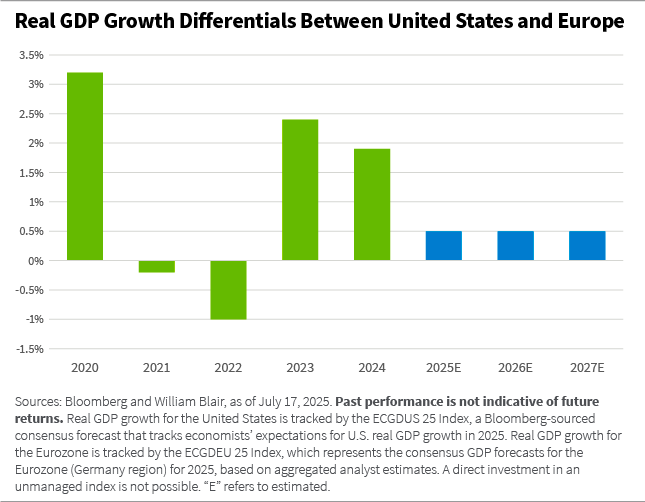

In a nutshell, gross domestic product (GDP) growth outside the United States has improved, particularly in the euro area, Japan, and China. Notably, the excess real GDP growth of the United States relative to Europe has meaningfully declined from more than 3% in 2020 on the back of significant COVID-related stimulus in the United States to 0.5% estimated excess growth over the next several years.

While it remains true that U.S. companies innovate and commercialize scientific breakthroughs particularly well, other countries are now moving to create conditions to help unlock domestic growth opportunities. What’s behind the shift?

Action and Reaction

In our opinion, a flurry of policy changes by the Trump administration has forced countries around the world to grapple with now-inescapable challenges: how to respond to a reduced, and more costly, U.S. security blanket; how to adjust to a new tariff regime from the world’s principal demand center; how to stay relevant in the age of artificial intelligence (AI); and more fundamentally, how to overcome stagnant or falling incomes (that have fueled political populism) without upending the global order that led to unprecedented peace and prosperity.

We believe policy responses to these challenges can be viewed as sources of economic growth.

We believe policy responses to these challenges can be viewed as sources of economic growth.

The United States has long spent more on defense than the next 10 North Atlantic Treaty Organization (NATO) members combined. The Russia-Ukraine war, coupled with the United States wavering to uphold its NATO commitments, jolted the European Union (EU) into ratcheting up its defense spending. Most members recently committed to elevate military and related spending to 5% of GDP, something that seemed unthinkable only a few years ago.

But why spend more to buy gear from an increasingly fickle partner? Europe is mobilizing funds and streamlining procurement to enable the rapid rise of its domestic defense industry. Even Germany finally shed its fiscal straitjacket and committed to spending at least €500 billion over the next decade to upgrade its infrastructure and military capabilities.

It is little wonder, then, that many new defense companies have sprung up in Europe over the last five years when the sector remained taboo for decades.

In addition, tariffs are back—even though they were widely seen as inimical to growth the last time they were used in earnest a century ago. Thus, when the goods a country sells to the world’s largest economy become more expensive at the stroke of a pen, it is forced to innovate and to seek out new markets.

Said another way, a new problem requires a new solution, which is a path that may lie through stronger domestic growth. For Europe, we believe that means removing internal barriers to trade and unleashing investment. And for China, we believe that means building out a social safety net to generate stronger domestic demand.

In our opinion, technological advancements underpin economic and political realignments as well. The rapid proliferation of AI capabilities is already redefining modern warfare and will soon be evident in healthcare and manufacturing. These changes will likely affect not only where we work, but whether we drive to get there, how we spend our leisure, and what we consume.

To enable these advancements, we think data centers need to become as ubiquitous as factories were 50 years ago. But supporting datacenters requires building out all the attendant additional electricity generation and related infrastructure necessary to connect and operate these facilities. In other words, more economic growth in most parts of the world will likely be spurred by investment into power generation and distribution.

A new problem requires a new solution, which is a path that may lie through stronger domestic growth.

Finally, underpinning these recent policy changes is the challenge of generating income growth in most modern, mature democracies.

Following the Global Financial Crisis (GFC), most countries, with the notable exception of the United States, embarked on a path of fiscal consolidation, which resulted in chronic underinvestment, anemic economic activity, and the rise of populism (which we also saw in the United States).

In response, the political class in most established democracies has prioritized economic growth as an antidote to economic stagnation and rising populism. Indeed, U.S. tariffs can be seen as a political response to the hollowing out of the middle class and market share loss to producers from other countries following decades of pro-globalization policy.

Exact policies are, of course, specific to local conditions. Japan continues to focus on improving capital allocation and corporate governance, with South Korea now looking to follow suit. China is stabilizing its real estate market and rolling out social services provisions where people live rather than where they’re registered (for those social services).

And in Europe, the report, “Towards a Genuine Economic and Monetary Union,” prepared under the leadership of former European Central Bank (ECB) President Mario Draghi, has been used as a policy blueprint to streamline intra-EU regulations so European domestic markets can grow and European companies can regain competitiveness.

Same As It Ever Was

The proliferation of economic growth as an outcome of solving current challenges is perhaps less surprising than meets the eye.

To answer the question, “why does growth happen?”, our global equity strategy team created a framework called the Perpetual Growth Machine (PGM). Its core thesis is that human beings want to improve their lot; they always have and always will, and so they’ll deploy ingenuity and resources toward developing new tools and new solutions. Growth, therefore, is the result.

The Perpetual Growth Machine’s core thesis is that human beings want to improve their lot; they always have and always will.

Acute problems generate solutions, and solutions to existing problems generate new challenges, which in turn must be overcome. We believe this process can result in economic growth.

The PGM is always on, identifying where people are trying to solve current problems, and we believe this will help point towards improving growth, potentially impacting asset price performance.

Hugo Scott‐Gall, partner, is the head of William Blair’s global equity team, on which he also serves as a portfolio manager.