December 12, 2023 | U.S. Growth and Core Equity

U.S. Onshoring and Its Impact on U.S.-Centric Companies

Rob Lanphier, Former Partner

Former Portfolio Specialist

Small-Mid Cap Generalist Analyst

December 12, 2023 | U.S. Growth and Core Equity

Rob Lanphier, Former Partner

Former Portfolio Specialist

Small-Mid Cap Generalist Analyst

View Fund:

https://im.williamblair.com/investments/mutual-funds/bgfix-growth-fund

View Fund:

https://im.williamblair.com/investments/mutual-funds/lcgfx-large-cap-growth-fund

View Fund:

https://im.williamblair.com/investments/mutual-funds/wbsix-small-cap-growth-fund

View Fund:

https://im.williamblair.com/investments/mutual-funds/wbcix-small-mid-cap-core-fund

View Fund:

https://im.williamblair.com/investments/mutual-funds/wsmdx-small-mid-cap-growth-fund

For thousands of years, civilization has benefited from some form of globalization. Historians may point to the establishment of the Silk Road in the 2nd century B.C.E. as the true initiation of trade from one region of the world to another.

But advancements in transportation, freedom of the seas, and global growth have driven demand for more diverse goods, often at considerably lower costs, and geographic diversification from a manufacturing risk-mitigation perspective. It has been a win-win for both consumers and commercial establishments. What could possibly go wrong?

In recent years, globalization has begun to slow down slightly, as supply chain disruptions, many of which started well before COVID-19, collided with an ever more demanding manufacturing and retail base that expected just-in-time (JIT) deliveries.

JIT is a supply chain strategy focused on minimal waste and maximum efficiency to reduce costs while satisfying immediate customer demands. Suppliers may be given a "delivery window" to meet, as well as an explicit volume of goods that are expected to be delivered. If either the time or the volume varies from the order placed, the supplier could be penalized.

With logistics and systems tracking commercial activity on a real-time basis, JIT can work for manufacturers, retailers, and suppliers. All are faced with inventory carrying costs that encourage lowering safety stock if JIT works as planned.

While the U.S. Federal Reserve’s (Fed) actions to raise interest rates and tighten lending will undoubtedly pressure economic growth, slow capital spending, and thus onshoring generally in the short run, we believe the secular trend of onshoring is indisputable.

Further, there are many reasons why supply chains began to fail despite advanced technology throughout the process. A few of the more important disruptive variables might include geopolitical tensions, tariffs, transportation and labor costs, intellectual property (IP) security, and incremental U.S. government financial incentives.

At the same time, U.S. manufacturers utilized enhanced productivity, embracing automation, robotics, software, and most recently, artificial intelligence (AI), to narrow the cost differential with lower-cost regions of the world. Terms like “friend-shoring” and “near-shoring” have also gained traction, but our focus will be on those companies transferring goods, components, materials, sub-assemblies, or IP back to the United States—specifically, a term we will refer to as “onshoring.”

In sum, providing product on time, on budget, and on spec is driving suppliers and retailers at every level to rethink their production and sourcing outside the United States, which is a shift that has the potential to benefit U.S. small- and mid-cap companies.

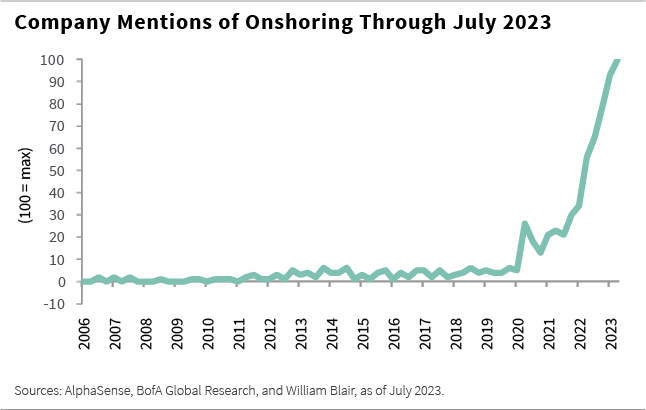

The chart below highlights U.S. companies that are formally using the term “onshoring” in their public filings. It shouldn’t come as a surprise that the concept gained traction because of COVID-19, but note that onshoring began well before the pandemic and has accelerated exponentially since then.

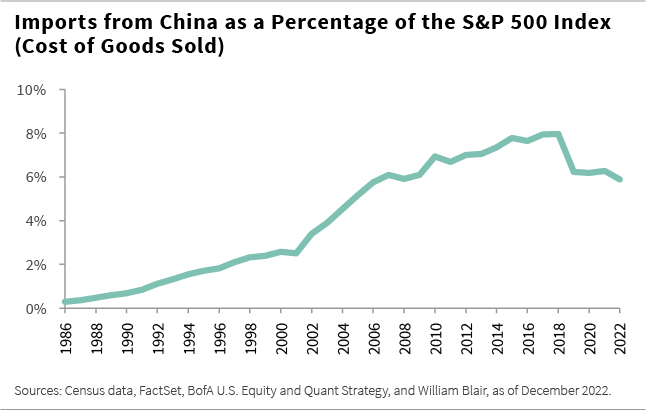

While the popularity of onshoring has grown, the opposite is true for some developing markets such as China, whose exports to the United States have slowed since 2017. Note too that the chart below only extends through 2022, but we expect that we likely will not see a reversal of this downward trend in 2023.

Numerous delays or cancellations of new U.S. investments into China, intensified Chinese regulatory scrutiny (concerning data access, personal information, and cyber security), and rising nationalism within China in recent years have exacerbated this exodus.

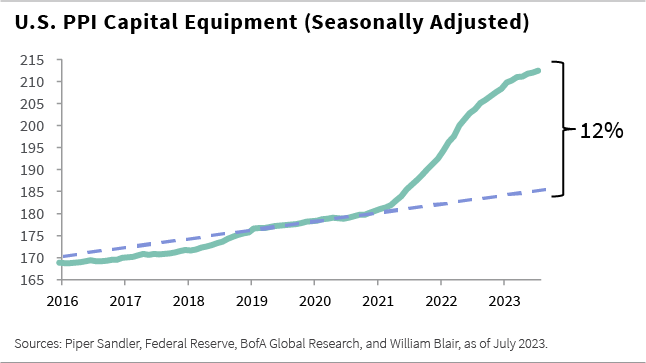

For U.S. onshoring to occur, we will likely need to see U.S. capital spending—and specifically, construction spending—to accelerate. It is particularly impressive to observe this pick-up in producer spending, shown in the chart below, considering that interest rates have been on the rise for the past two years.

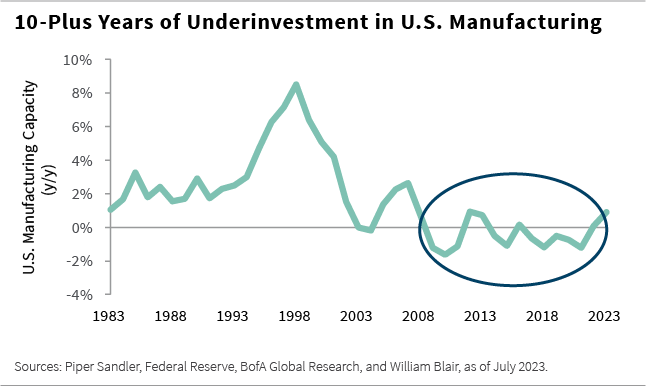

When observed over a longer period, what should be apparent is the underinvestment seen in U.S. manufacturing since the Global Financial Crisis, which accentuates the more recent spending required, as shown in the chart below.

In addressing the duration of onshoring, it is important to ask three key questions about supply chains: are they cost effective, do they mitigate risk, and what is the level of confidence and trust in their reliability and sustainability.

We have pointed out that U.S. technological and productivity improvements continue to evolve, often narrowing the previous cost advantages of developing or emerging economies while labor costs abroad have often materially risen.

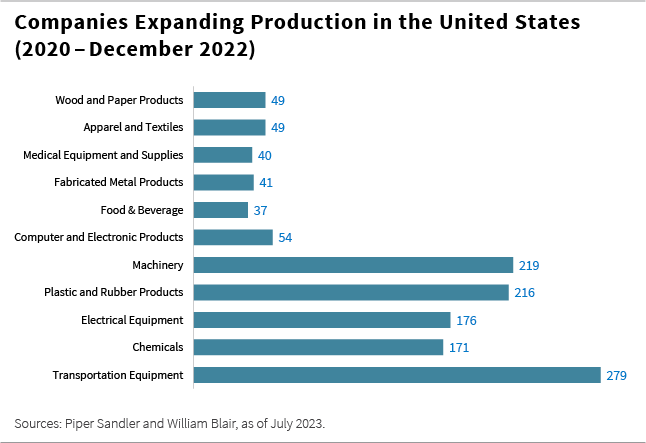

The breadth of industries undertaking onshoring initiatives is impressive, as shown in the chart below.

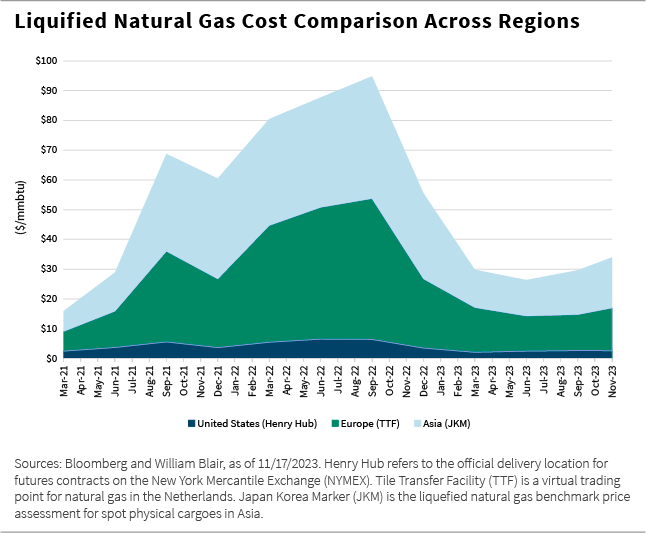

What too often is overlooked by investors in our opinion is the enormous cost advantage that the United States holds from an energy perspective. As the chart below demonstrates, U.S. manufacturers that rely on natural gas as an input cost are structurally advantaged in comparison to foreign competitors. Following Russia’s invasion of Ukraine, this energy cost advantage has further increased even after the initial energy price spikes in Europe and Asia have subsided. As of the time of this writing, U.S. companies are only paying $2.50 to $3.00 per 1 million British thermal units (MMBtu), while their peers in Europe and Asia are paying $14 to $16 per MMBtu.

Recent U.S. legislation creating incentives and subsidies for strategic industries has proven to be a further accelerant to onshoring, including the CHIPS and Science Act, the Inflation Reduction Act, and the Defense Production Act. While the Fed’s actions to raise interest rates and tighten lending will undoubtedly pressure economic growth, slow capital spending, and thus onshoring generally in the short run, we believe the secular trend of onshoring is indisputable.

While the media and Wall Street have largely ignored the benefits of onshoring beyond the companies transitioning, the reality is that capital spending on the factories being built represents a fraction of the total spend when considering the surrounding infrastructure that is often required. Roads and services—both public and private—may meaningfully create or expand communities.

We believe local companies are likely to disproportionately benefit because of their flexibility to adapt and respond quickly. This is a distinctive tailwind for small and midsize companies that we expect will play out over many years.

Providing product on time, on budget, and on spec is driving suppliers and retailers at every level to rethink their production and sourcing outside the United States, which is a shift that has the potential to benefit U.S. small- and mid-cap companies.

One mid-cap quality U.S. company that we expect to benefit from onshoring is a leader in rock quarries. While it may seem like a commodity business, this company deals in aggregates such as rocks, sand, and gravel. These materials are expensive to transport given their weight, and thus local oligopolies are created around these quarries. Whether it is roads, bridges, or concrete production that is required, only those geographically close to the customer are likely able to price competitively.

Another potential U.S. onshoring beneficiary is a leader in the production and distribution of high-density polyethylene (HDPE) pipe, which are used in stormwater and sanitary sewer applications and offer several advantages over traditional concrete piping. Because HDPE pipe is lighter, easier to install, and erosion-resistant relative to concrete, this company appears poised to enjoy a significant tailwind as capital spending continues to ramp up.

As onshoring continues to reshape the global trade landscape, it is crucial for investors to understand its impact. We believe our focus on bottom-up investing allows us to better appreciate the secular trends impacting U.S. companies while identifying those that may specifically benefit from onshoring, as described above, providing us with a longer-term investment edge.

Rob Lanphier is a former partner and former portfolio specialist on William Blair’s U.S. growth and core equity team.

Jim Jones, CFA, partner, is a portfolio manager on William Blair’s U.S. growth and core equity team.

View Fund:

https://im.williamblair.com/investments/sicav-funds/lu2511384518-us-large-cap-growth-fund

View Fund:

https://im.williamblair.com/investments/sicav-funds/lu0995404869-us-all-cap-growth-fund

View Fund:

https://im.williamblair.com/investments/sicav-funds/lu1890055632-us-small-mid-cap-core-fund

View Fund:

https://im.williamblair.com/investments/sicav-funds/lu0995404943-us-small-mid-cap-growth-fund

View Strategy:

https://im.williamblair.com/investments/separate-accounts/all-cap-growth

View Strategy:

https://im.williamblair.com/investments/separate-accounts/large-cap-growth

View Strategy:

https://im.williamblair.com/investments/separate-accounts/small-cap-growth

View Strategy:

https://im.williamblair.com/investments/separate-accounts/small-mid-cap-core

View Strategy:

https://im.williamblair.com/investments/separate-accounts/small-mid-cap-growth

Want the latest insights on the economy and other forces shaping the investment landscape?

Subscribe to our Investing Insights newsletter.

Any investment or strategy mentioned herein may not be appropriate for every investor. There can be no assurance that investment objectives will be met. Products and services listed are available only to residents of this jurisdiction and may only be available to certain categories of investors. The information on this website does not constitute an offer for products or services, or a solicitation of an offer to any persons outside of this jurisdiction who are prohibited from receiving such information under applicable laws and regulations. Nothing on this webpage should be construed as advice and is therefore not a recommendation to buy or sell shares.

Please carefully consider the William Blair Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus and summary prospectus, which you may obtain by calling 1-800-742-7272. Read the prospectus and summary prospectus carefully before investing. Investing includes the risk of loss.

The William Blair Funds are distributed by William Blair & Company, L.L.C., member FINRA/SIPC.

The William Blair SICAV is a Luxembourg investment company with variable capital registered with the Commission de Surveillance du Secteur Financier (“CSSF”) which qualifies as an undertaking for collective investment in transferable securities (“UCITS”). The Management Company of the SICAV has appointed William Blair Investment Management, LLC as the investment manager for the fund.

Please carefully consider the investment objectives, risks, charges, and expenses of the William Blair SICAV. This and other important information is contained in the prospectus and Key Investor Information Document (KIID). Read these documents carefully before investing. The information contained on this website is not a substitute for those documents or for professional external advice.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets and frontier markets. Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Different investment styles may shift in and out of favor depending on market conditions. Diversification does not ensure against loss.

Past performance is not indicative of future returns. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security.

William Blair Investment Management, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission.

Issued in the United Kingdom by William Blair International, Ltd., authorized and regulated by the Financial Conduct Authority (FCA), and is only directed at and is only made available to persons falling within articles 19, 38, 47, and 49 of the Financial Services and Markets Act of 2000 (Financial Promotion) Order 2005 (all such persons being referred to as "relevant persons").

Issued in the European Economic Area (EEA) by William Blair B.V., authorized and supervised by the Dutch Authority for the Financial Markets (AFM) under license number 14006134 and also supervised by the Dutch Central Bank (DNB), registered at the Dutch Chamber of Commerce under number 82375682 and has its statutory seat in Amsterdam, the Netherlands. This material is only intended for eligible counterparties and professional clients.

Issued in Switzerland by William Blair Investment Services (Zurich) GmbH, Talstrasse 65, 8001 Zurich, Switzerland ("WBIS"). WBIS is engaged in the offering of collective investment schemes and renders further, non-regulated services in the financial sector. WBIS is affiliated with FINOS Finanzomubdsstelle Schweiz, a recognized ombudsman office where clients may initiate mediation proceedings pursuant to articles 74 et seq. of the Swiss Financial Services Act ("FinSA"). The client advisers of WBIS are registered with regservices.ch by BX Swiss AG, a client adviser registration body authorized by the Swiss Financial Market Supervisory Authority ("FINMA"). WBIS is not supervised by FINMA or any other supervisory authority or self-regulatory organization. This material is only intended for institutional and professional clients pursuant to article 4(3) to (5) FinSA.

Issued in Australia by William Blair Investment Management, LLC (“William Blair”), which is exempt from the requirement to hold an Australian financial services license under Australia's Corporations Act 2001 (Cth). William Blair is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and regulated by the SEC under the U.S. Investment Advisers Act of 1940, which differs from Australian laws. This material is intended only for wholesale clients.

Issued in Singapore by William Blair International (Singapore) Pte. Ltd. (Registration Number 201943312R), which is regulated by the Monetary Authority of Singapore under a Capital Markets Services License to conduct fund management activities. This material is intended only for institutional investors and may not be distributed to retail investors.

Issued in Canada by William Blair Investment Management, LLC, which relies on the international adviser exemption, pursuant to section 8.26 of National Instrument 31-103 in Canada.

The content contained in this site is intended as informational or educational in nature and does not constitute investment advice or a recommendation of any investment strategy or product for a particular investor. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions. Investors should consult a financial professional/financial consultant or investment adviser before making any investment decisions. Investing includes the risk of loss.

Copyright © 2026 William Blair. William Blair is a registered trademark of William Blair & Company, L.L.C. “William Blair” refers to William Blair Investment Management, LLC and affiliates.